Above is a screenshot of my current insurance auto policy on the progressive web app. In this article I will try to provide insight into 1) What each coverage means and 2) Why I made the decision to purchase that amount of coverage. *Remember that the proper coverage for you will be very fact specific and may not necessarily match what I have selected below. I will try to discuss different outcomes from each selection.

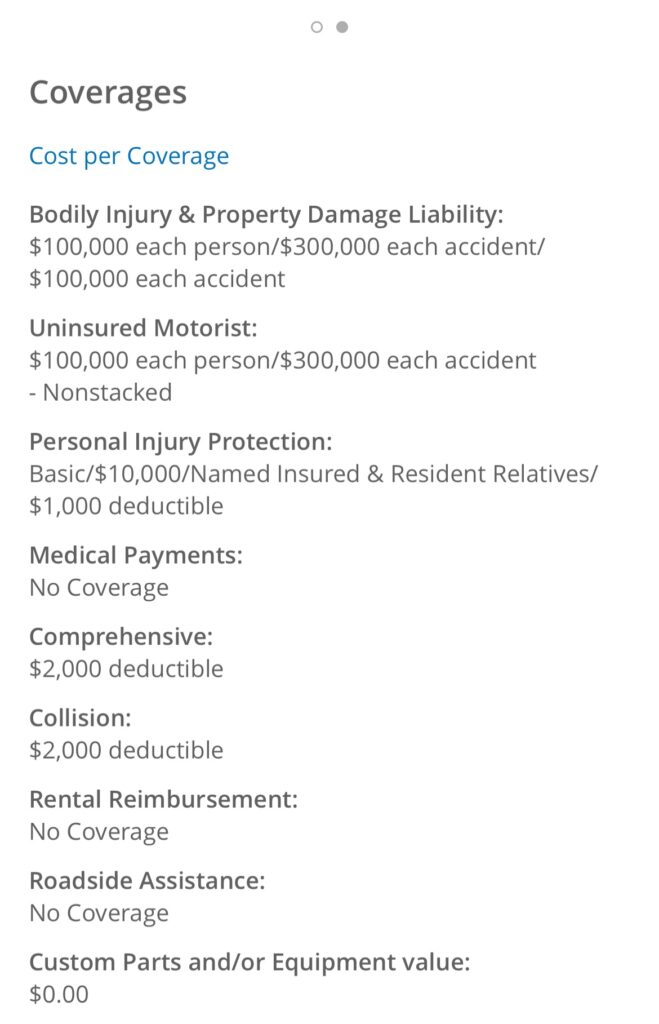

Type 1: Bodily Injury & Property Damage

The first type of coverage on this list is called Bodily Injury & Property Damage Liability. We will break this down into two separate types: 1) Bodily Injury and 2) Property Damage. The first type, bodily injury, deals with medical bills that are suffered by another party when you are at fault for the accident. (If you are not at fault for the accident then the other driver cannot recover against you). This coverage protects your personal assets from being seized as compensation for injuries that you caused. Many individuals do not have high amounts for this type of coverage. In fact, up to 20 percent of Florida drivers have none of this type of coverage because it is not required by Florida law.

This means that if I were to get in an accident where I was at fault for the accident, the other driver could potentially recover $100,000 for each person injured by my conduct. The $300,000 each accident coverage means that the maximum recoverable against my insurance would be $300,000 if up to three people were hurt in the vehicle.

The second part, 2) Property damage would allow for $100,000 to repair another party’s vehicle and should be more than enough to cover against over 95% of the cars in the road.

Why Is This Type of Coverage Important?

This coverage protects my personal assets from being seized as compensation for an accident that I was at fault for. It will require that an insurance company defend me against a lawsuit from another driver who sues me for their injuries or property damage. All things being equal, usually it is a good idea to carry enough coverage to protect your personal assets. That is because once an insurance company settles a case on your behalf, the plaintiff will sign what is called a release of liability, that will prevent them from collecting from other tortfeasors (you) for the injuries they suffered in that accident. This means that someone seeking recovery from you would much rather go after a larger insurance policy than an individual’s personal assets that would involve a lot more risk to recover from.

Type 2: Uninsured Motorist

Next, we will look at the Uninsured Motorist Coverage (UM). I cannot understate enough how important this type of coverage is! Without this type of coverage, you are completely rolling the dice on the other driver having adequate Bodily Injury Coverage to cover you for your medical expenses if they are at fault for the accident. You can only purchase UM for up to the amount of your bodily injury coverage. It is a good idea to strive to have at least $100,000 in coverage. This will allow the average person to receive medical treatment for their injuries in the event they are hurt in a car crash.

Next, we will look at the Uninsured Motorist Coverage (UM). I cannot understate enough how important this type of coverage is! Without this type of coverage, you are completely rolling the dice on the other driver having adequate Bodily Injury Coverage to cover you for your medical expenses if they are at fault for the accident. You can only purchase UM for up to the amount of your bodily injury coverage. It is a good idea to strive to have at least $100,000 in coverage. This will allow the average person to receive medical treatment for their injuries in the event they are hurt in a car crash.

Type 3: Personal Injury Protection (PIP)

Personal Injury Protection is a type of Florida specific coverage that covers up to $10,000 worth of medical treatment, regardless of fault in the accident. This means, that even if you caused the accident yourself, you could still receive up to $10,000 of treatment. You will only be responsible for covering the deductible and a 20% reimbursement to the PIP carrier (unless you have Medical Pay Coverage – see below).

Type 4: Medical Pay

The last type of coverage that I will discuss in this article is called Medical Payments or “Med Pay” for short. This type of coverage will pay back the 20% that you are responsible for when paying back a PIP carrier. For most people this type of coverage is not as important as Bodily Injury or Uninsured Motorist and is much less commonly carried. That is because, you will need to reimburse Med Pay from any settlement proceeds you receive when collect from another driver’s bodily injury or your own uninsured motorist.

Conclusion:

Remember that the information discussed above is not meant to be legal advice. Every individual policy should be carefully gone over with an attorney if an individual is not sure about the best choice for each type of coverage. Only an experienced personal injury attorney can fully explain the implications of your choices and how it will impact you if you are in an accident.

The Harris Team

Ⓒ 2021 Harris Law Group

All Rights Are Reserved